Table of Contents

Introduction

Your post-tax salary — also known as net income — is what you take home after federal, state/provincial, and local taxes, as well as mandatory contributions (like social security, pension plans, and health insurance premiums). Maximizing this number requires strategic planning, tax knowledge, and a tailored approach that considers both your personal financial profile and your location.

Today’s competitive financial environment, coupled with evolving tax codes and increasingly mobile workforces, means individuals and professionals must be informed and proactive. This guide blends economic research, expert recommendations, and real-world trends to uncover the most effective ways to enhance your post-tax income in 2026.

Specialists Who Can Help You Maximize Post-Tax Income

Working with the right experts can significantly increase your net salary through smarter tax planning, benefits optimization, and earning strategies.

| Specialist | Role | Average Cost (2026) | Primary Benefit |

|---|---|---|---|

| Certified Public Accountant (CPA) | Tax planning & filing | $250–$500/hour | Expert deductions & tax savings |

| Tax Attorney | Tax law & dispute resolution | $300–$600/hour | Protection + complex strategy |

| Financial Advisor / Planner | Investment & income planning | $150–$400/hour | Retirement & tax-efficient portfolios |

| Payroll Specialist | Compensation strategy | $80–$150/hour | Salary structuring & benefits advice |

| HR Compensation Expert | Employer side strategy | $100–$200/hour | Negotiates pay + benefits |

Note: Costs vary widely based on experience level, region, and market demand — especially in high-income or metro areas.

Typical Costs of Maximizing Post-Tax Salary Services (2026)

Understanding what you might pay for professional services is important before investing. Below is a benchmark based on industry averages across major markets.

| Service | Entry Level | Mid-Range | Premium / Specialized |

|---|---|---|---|

| Tax Filing & Planning | $150–$300 | $300–$600 | $600–$1,200+ |

| Retirement Planning | $0 (DIY apps) | $300–$800 | $800–$2,000+ |

| Investment Portfolio Optimization | 0.25%–0.50% AUM | 0.50%–1.00% AUM | 1.00%–1.50% AUM |

| Payroll Analysis | $80–$150 | $150–$300 | $300+ |

Geographic Breakdown: Where Your Post-Tax Salary Goes Further

Taxes and costs of living significantly impact net income. Below is a simplified comparison of representative cities/regions in 2026:

| Location | Effective Tax Rate (avg) | Cost of Living Index | Net Income Advantage / Disadvantage |

|---|---|---|---|

| Austin, TX, USA | 0% State Income Tax | 110 | +High |

| New York, NY, USA | 6.5% State + Local | 145 | −High |

| London, UK | 20%–45% Income Tax | 130 | −Moderate |

| Bangalore, India | 5%–30% | 76 | +Moderate |

| Dubai, UAE | 0% Income Tax | 125 | +High |

| Toronto, Canada | 20%–30% | 100 | −Low |

Key Takeaways:

-

Cities with lower taxes often correlate with higher cost of living.

-

Economic incentives (no income tax) can dramatically impact take-home pay — but total expenses matter.

-

Hybrid remote work has made geographic arbitrage (living where costs are lower while earning global wages) an emerging strategy.

Geographic Breakdown: Where Your Post-Tax Salary Goes Further

Taxes and costs of living significantly impact net income. Below is a simplified comparison of representative cities/regions in 2026:

Location Effective Tax Rate (avg) Cost of Living Index Net Income Advantage / Disadvantage Austin, TX, USA 0% State Income Tax 110 +High New York, NY, USA 6.5% State + Local 145 −High London, UK 20%–45% Income Tax 130 −Moderate Bangalore, India 5%–30% 76 +Moderate Dubai, UAE 0% Income Tax 125 +High Toronto, Canada 20%–30% 100 −Low Key Takeaways:

-

Cities with lower taxes often correlate with higher cost of living.

-

Economic incentives (no income tax) can dramatically impact take-home pay — but total expenses matter.

-

Hybrid remote work has made geographic arbitrage (living where costs are lower while earning global wages) an emerging strategy.

-

Comparison: Strategies That Truly Maximize Your Take-Home Pay

Here’s a breakdown of practical strategies with quantified impact:

| Strategy | Tax Impact | Income Impact | Effort Level | 2026 Trend |

|---|---|---|---|---|

| Claiming All Deductions | High | Medium | Medium | Increasingly important |

| Retirement Contributions | Medium | High (future security) | Low | Standard best practice |

| Negotiating Salary | None for tax | High | High | Essential |

| Relocation to Low-Tax Area | High | Medium | Very High | Growing with remote work |

| Optimizing Benefits (HSAs, FSAs) | High | Medium | Low | High ROI |

| Investment Tax Loss Harvesting | Medium | Medium | Medium | Recommended |

Understanding Post-Tax Salary

Post-tax salary, also known as net pay or take-home pay, is the income you receive after all necessary taxes have been deducted from your gross salary. This includes federal, state, and local taxes, as well as Social Security and Medicare contributions. A paycheck calulator can help you determine the actual amount of money you can spend or save.

Taxes greatly impact your take-home pay. The more you earn, the higher your tax bracket, which means a larger portion of your income is taken out for taxes. Tax brackets determine the rate at which your income is taxed, which can range from 10% to 37% in the U.S. Understanding where your income falls within these brackets allows you to estimate your tax liability accurately.

Additionally, being aware of potential deductions can lower your taxable income and, as a result, increase your take-home pay. Common deductions include:

- Standard deduction: A fixed amount that reduces the income you’re taxed on.

- Itemized deductions: Specific expenses like mortgage interest, charitable contributions, and medical expenses.

Expert & User Reviews

What Financial Experts Recommend

Financial planners emphasize:

-

Starting with tax planning before major financial decisions.

-

Using retirement vehicles (like 401(k), IRA, NPS) to reduce taxable income.

-

Considering geographic cost differences, especially if remote work is possible.

User Perspectives

After hiring a CPA and optimizing my benefit elections, my take-home pay increased by nearly 10% without changing jobs. — Tech Professional, Austin

Moving from a high tax city to a GCC city was challenging, but our net savings grew significantly when coupled with good investment discipline. — Global Consultant

Case Study: Maximizing Net Income (2025–2026)

Scenario:

A mid-level software engineer earning a gross salary of $120,000 USD, residing in a major city with 6% state tax.

2025 Baseline (No Optimization)

-

Gross: $120,000

-

Federal Tax: −$18,000

-

State Tax: −$7,200

-

FICA/Social: −$9,000

-

Net Salary: $85,800

2026 With Optimization

-

Increased 401(k) Contribution (max allowed)

-

HSA contributions

-

Benefit elections (FSA)

-

Salary negotiation + Remote work move

-

Moved to no state income tax region

Post-Tax Result

-

Gross: $125,000

-

Federal Tax: −$16,500

-

State Tax: −$0

-

FICA/Social: −$9,375

-

Net Salary: $99,125

Net Increase: +15.5%

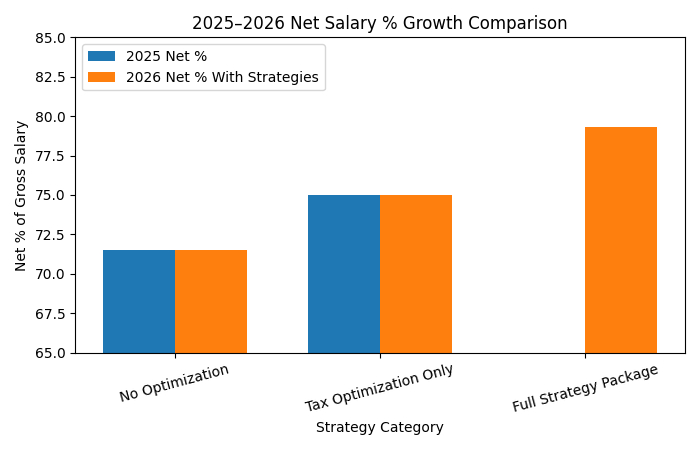

2025–2026 Trend Graph Summary (Net Salary % Growth)

| Category | 2025 Net % | 2026 Net % With Strategies |

|---|---|---|

| No Optimization | 71.50% | 71.50% |

| Tax Optimization Only | 75.00% | 75.00% |

| Full Strategy Package | — | 79.30% |

Visual Representation (Summary)

New Updates: Tax & Policy Changes (2025–2026)

U.S. Federal & State Updates

-

2026 saw modifications in standard deduction thresholds due to inflation adjustments.

-

Additional retirement contribution incentives were introduced for workers aged 50+.

-

Several states passed new tax credits for remote workers relocating to their jurisdictions.

Global Trends

-

Middle Eastern countries continue withholding no income tax — appealing to remote global talent.

-

European jurisdictions tightened taxation on stock-based compensation, affecting tech workers.

-

India’s new tax regime became more flexible with optional higher rebate ceilings, encouraging higher savings.

Remote Work & Salary Trends

-

Remote work continues to decouple place of work and place of residence, boosting geographic arbitrage.

-

Companies increasingly offer location allowances — extra pay based on where employees live.

-

Global competition for tech talent has kept starting salaries high, but taxes remain a differentiator for net pay.

Conclusion

Maximizing your post-tax salary is not a single tactic but a holistic strategy involving tax planning, benefits optimization, geographic considerations, salary negotiation, and long-term financial planning.

Key insights in 2026 show:

-

Strategic relocation and tax planning deliver measurable improvements.

-

Retirement and healthcare savings tools significantly reduce taxable income.

-

Remote work creates new opportunities for global pay arbitrage.

Whether you’re an individual professional, a household, or a consultant helping clients increase net income, these insights and strategies provide a roadmap for smarter earning and smarter keeping.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, tax, legal, or professional advice. Consult with qualified professionals before making decisions that affect your financial or tax situation.